July 2022 High-Line Metrics (proportion change from July 2019)

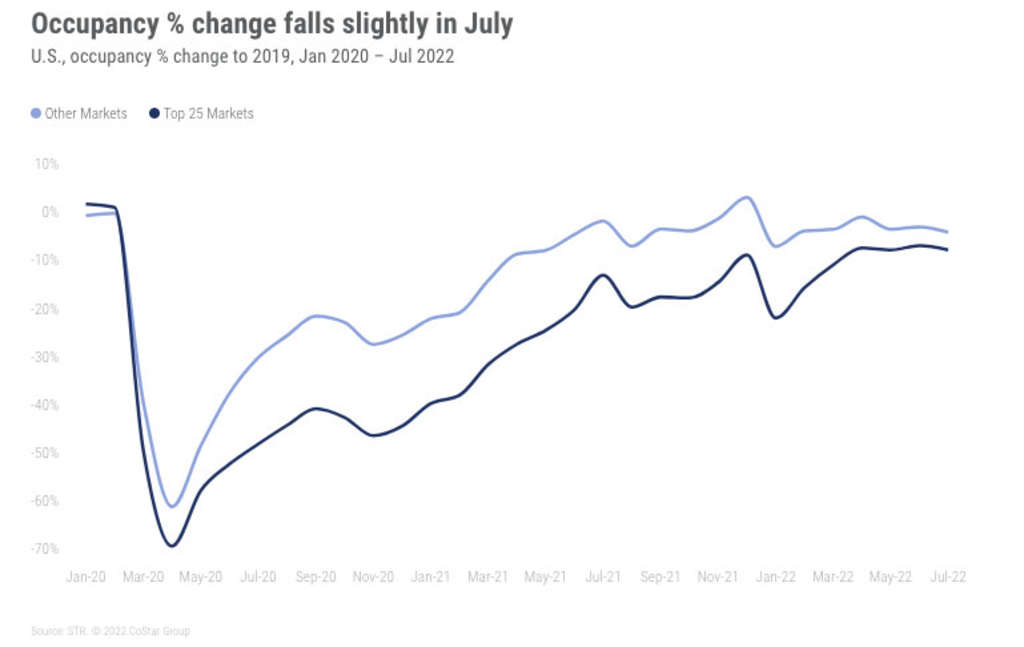

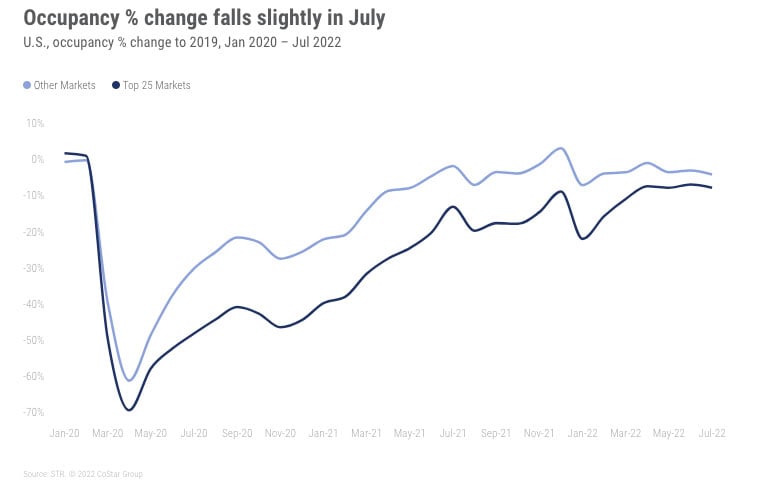

- Occupancy: 69.6% (-5.4%)

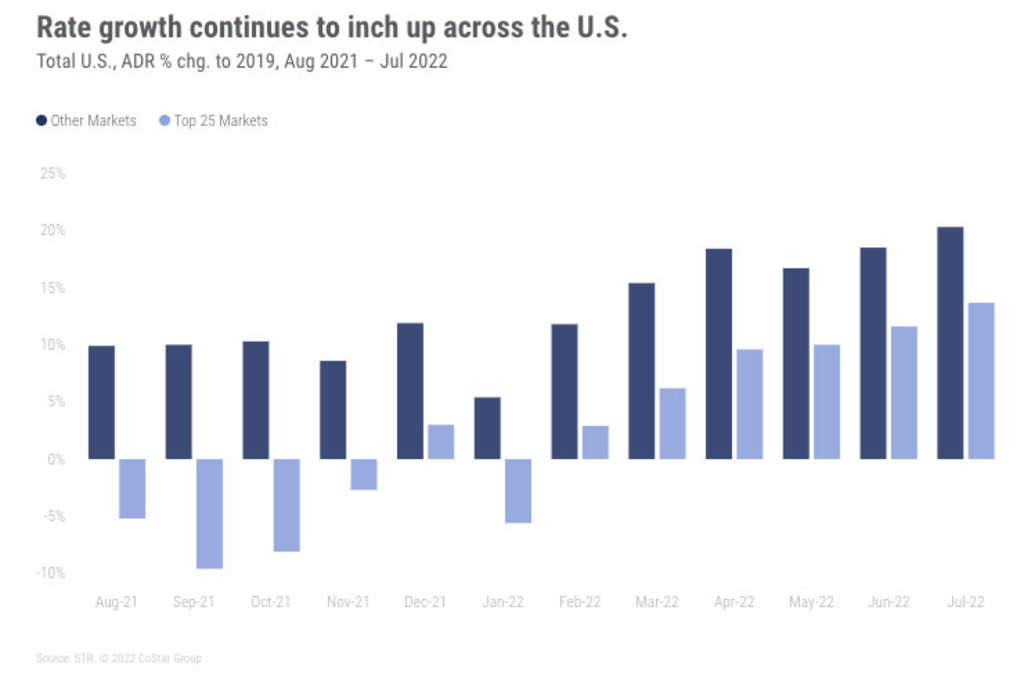

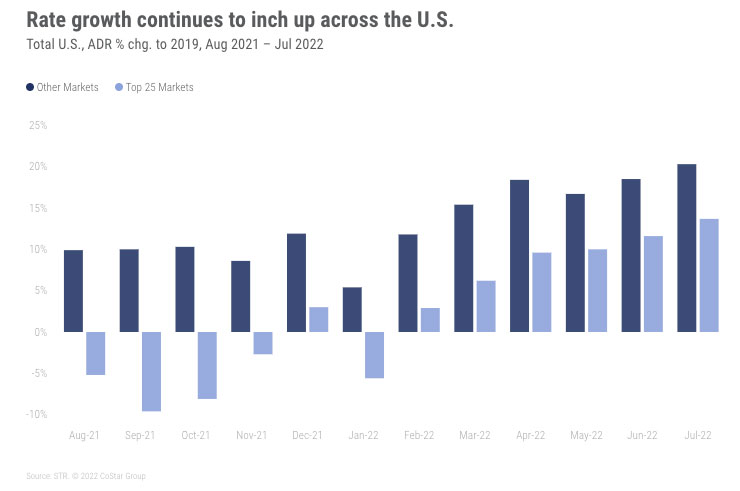

- Common each day fee (ADR): US$159.08 (+17.5%)

- Income per accessible room (RevPAR): US$110.73 (+11.2%)

Key factors from the month:

- Occupancy (absolute and index) declined month over month whereas ADR and RevPAR continued to rise.

- Actual ADR (inflation-adjusted) was almost 2% above the pre-pandemic comparable.

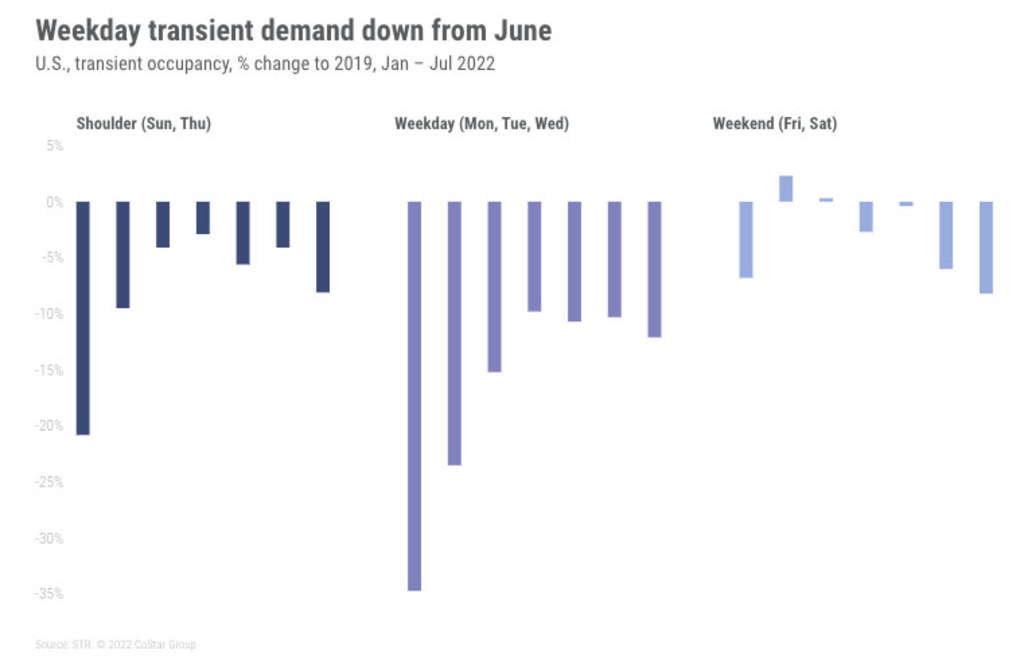

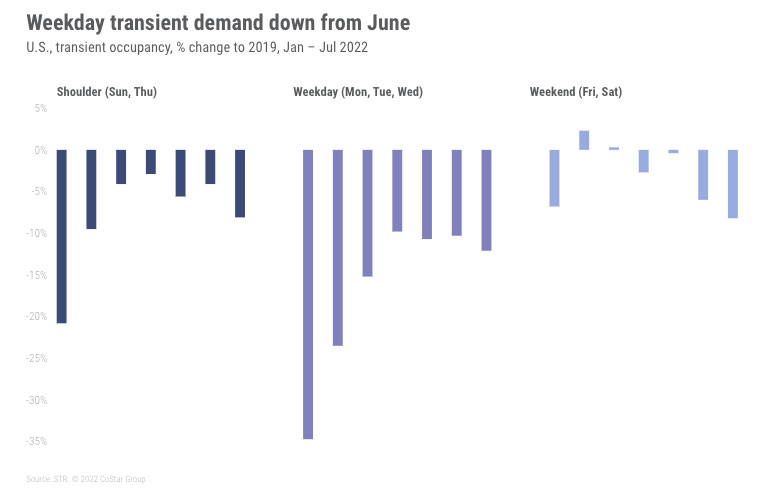

- Decrease weekend occupancy was the most important contributor to softened July occupancy.

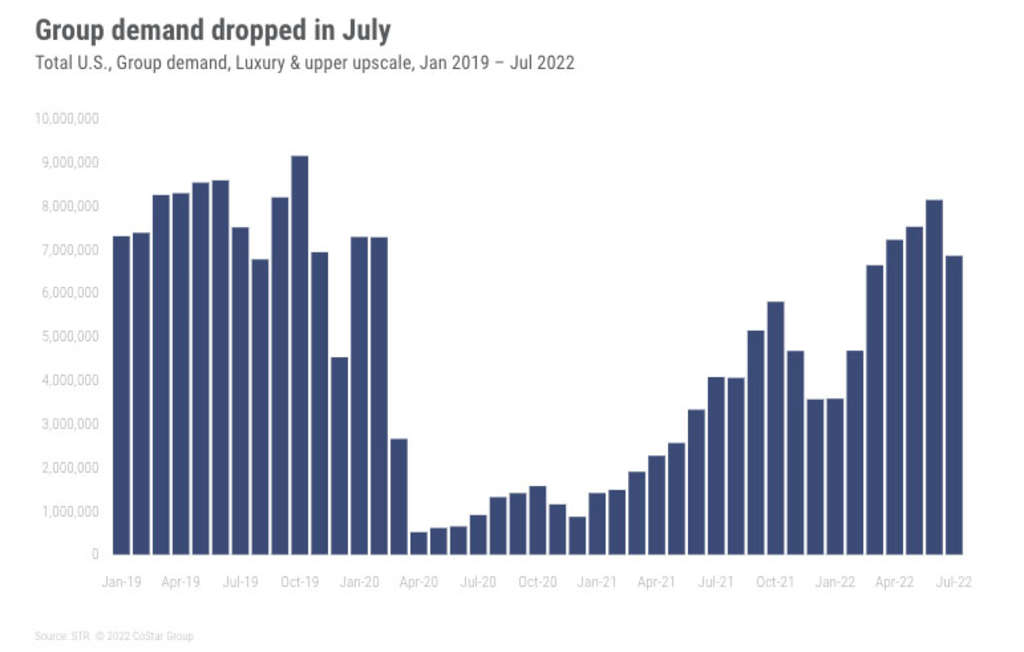

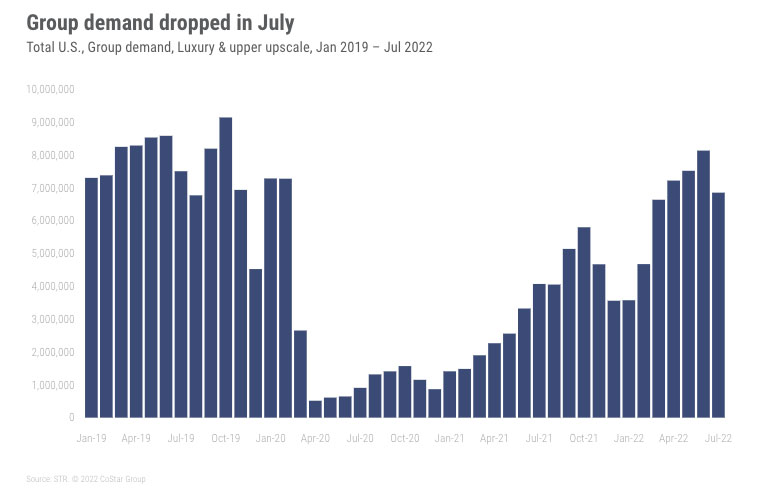

- Group demand dropped month over month due to much less weekend teams, though weekday teams continued to enhance.

- Regardless of softened weekend occupancy nationally, leisure-based markets reported the very best occupancy within the High 25 Markets and the very best demand development nationwide.

- The variety of rooms in building continued a downward trajectory.

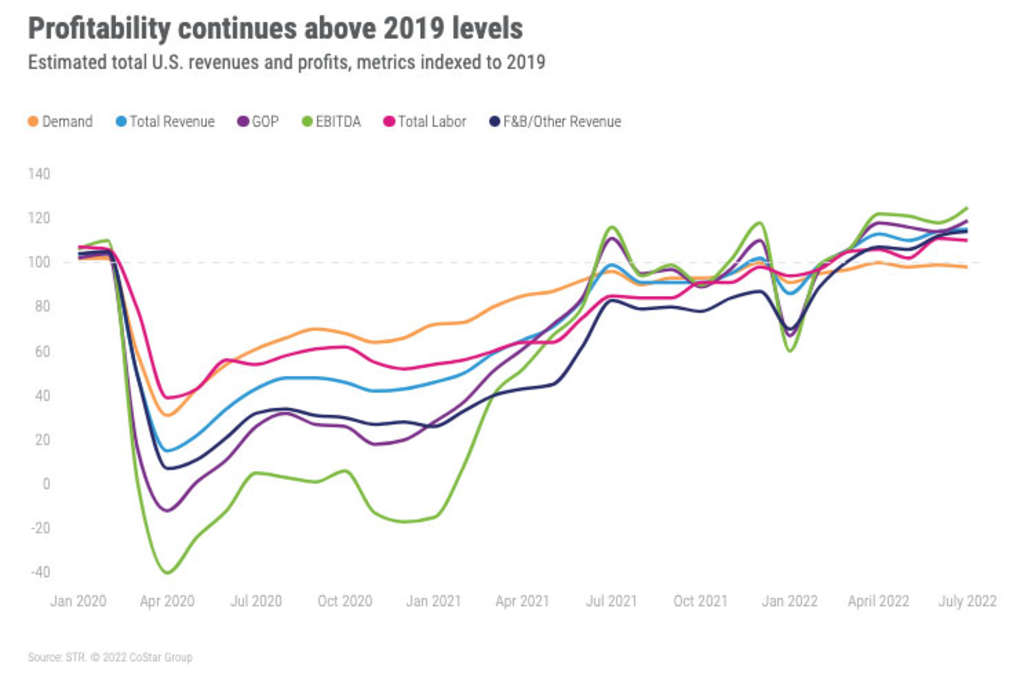

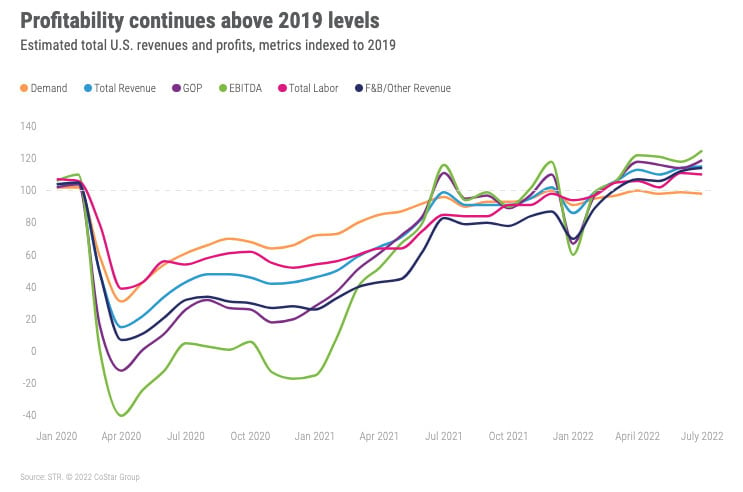

- U.S. resort GOPPAR exceeded the pre-pandemic comparable for a fourth consecutive month. Every of the important thing bottom-line metrics, nonetheless, decreased barely from June, whereas whole income elevated with peak summer time room demand and revenues.

Segmentation

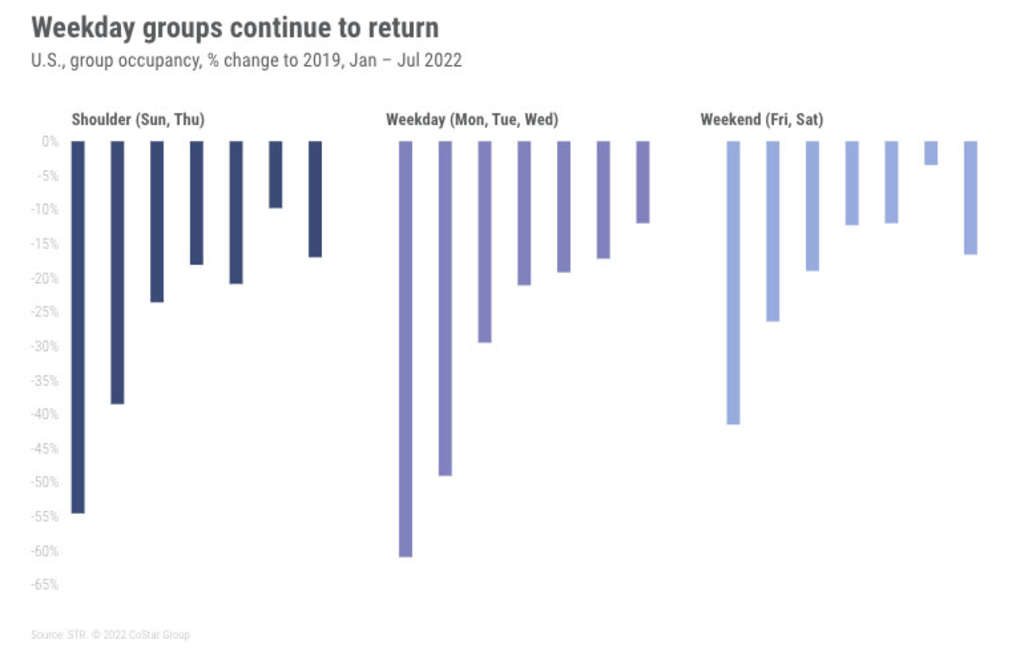

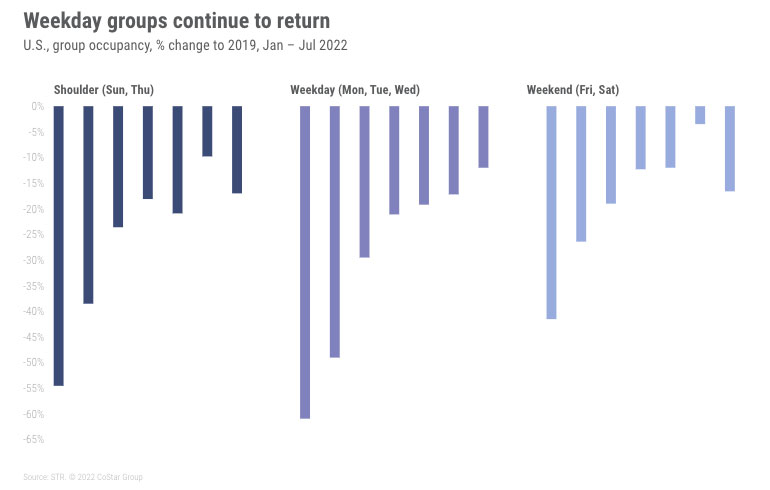

Group fell when whole demand and at demand indices to 2019.

Particularly, leisure-based weekend teams got here in noticeably decrease.

There could be some (weekend) group fatigue as calendars begin clearing out all of the postponed/rescheduled group occasions. Weekend group restoration began round this time final 12 months, so it’s attainable that weekends are slowing because the calendar normalizes.

Weekend transient demand additionally fell, one other signal pointing to diminished leisure demand. The transient weekday occupancy index dipped marginally month over month.

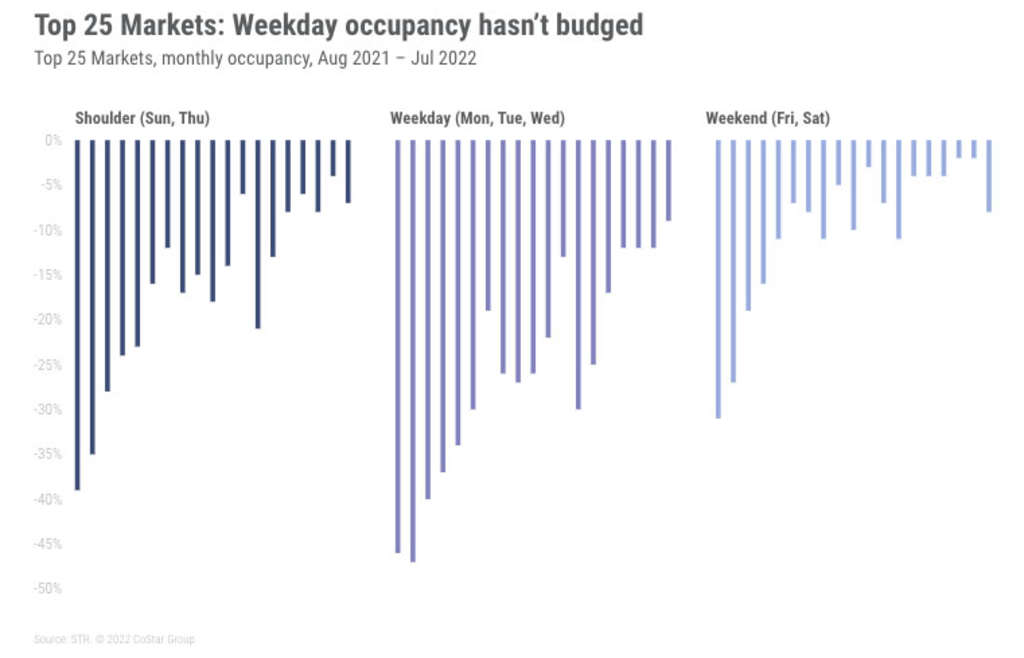

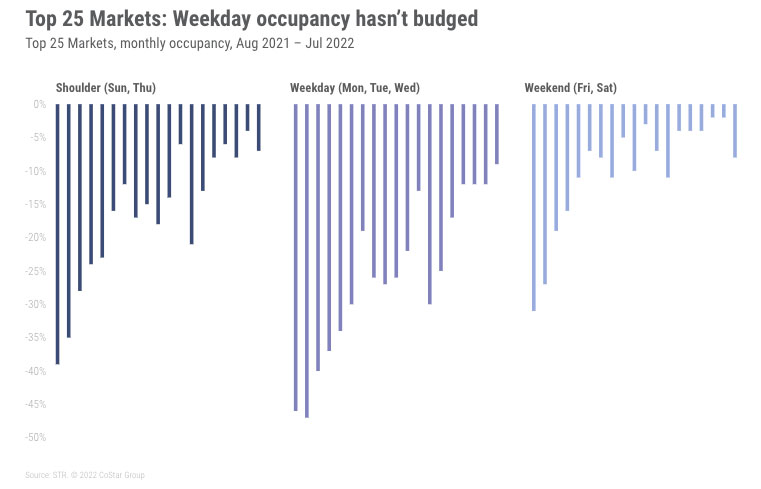

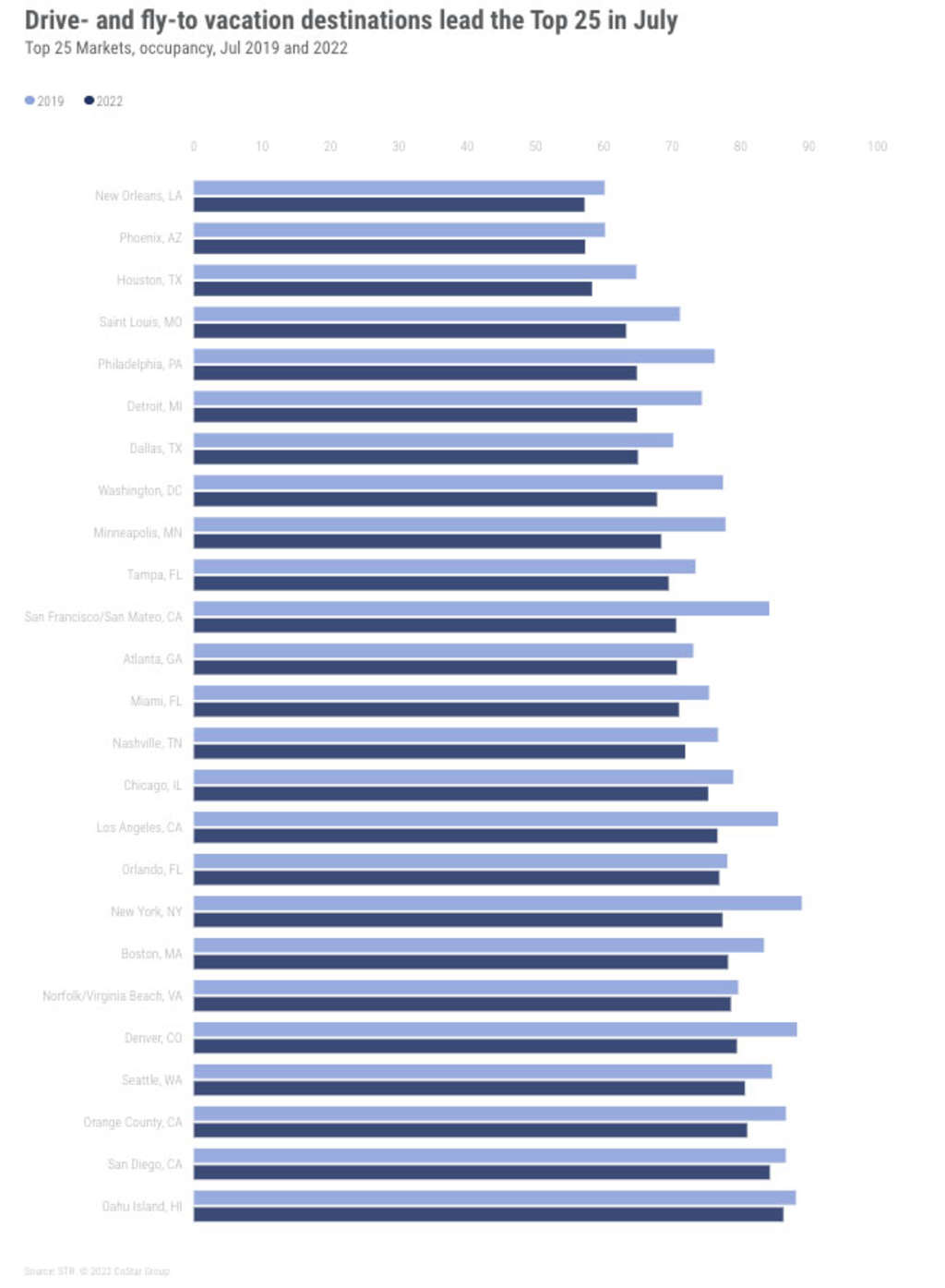

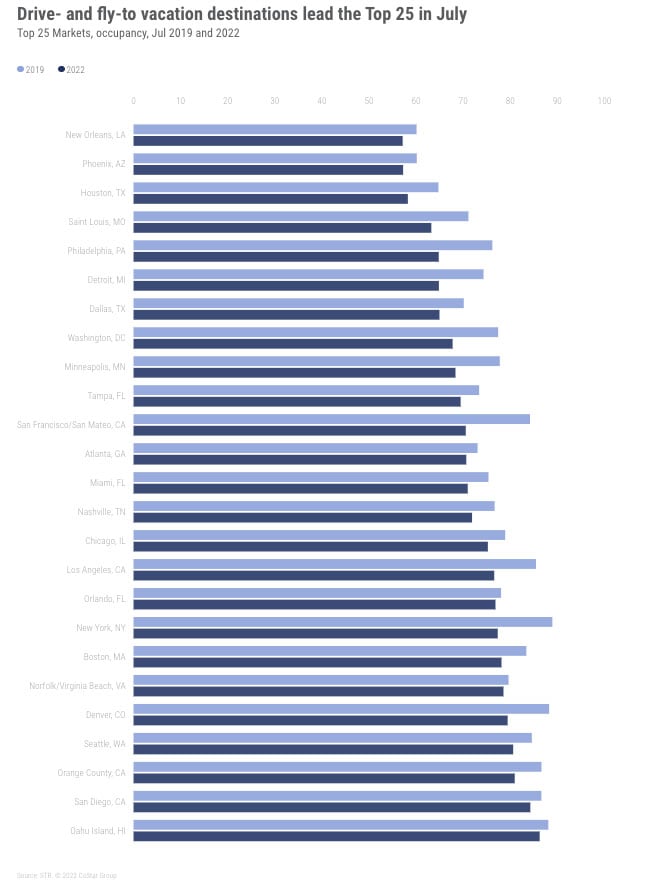

High 25 Markets

Enterprise journey restoration stays firmly plateaued within the High 25 Markets.

Restricted enterprise journey is extra possible a results of inflation than COVID at this level.

Friday and Saturday occupancy continued to say no, and occupancy indices fell throughout each the High 25 and all different markets.

Of the 166 STR-defined U.S. markets, 64, together with six High 25 Markets, reported demand above 2019 ranges whereas 93 markets reported demand indices at or higher than the nationwide common.

Florida continues to be well-represented throughout the top-performing markets in addition to secondary and tertiary southern cities. There’s a case to be made for each enterprise and leisure demand coming into the likes of Charleston, Charlotte, Knoxville, Austin, and Savannah.

Regardless of the softer weekend occupancy, summer time vacationers completely hit the High 25 Markets in July. Oahu, San Diego (drive-to), Orange County (Disneyland), and Norfolk (drive-to) all posted the very best occupancy months. Seattle, Denver, Boston, and New York Metropolis additionally gained occupancy.

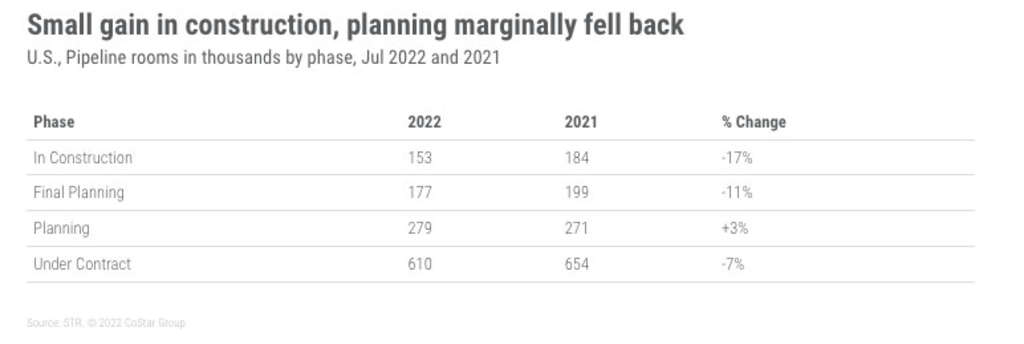

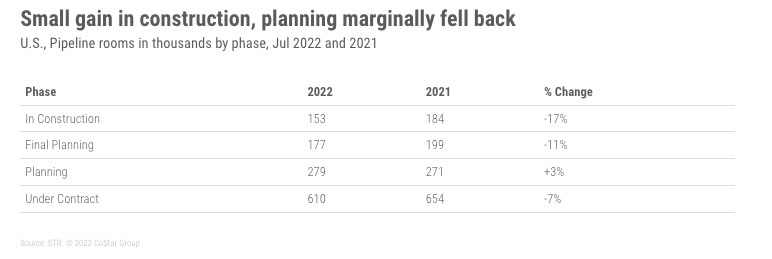

Pipeline

Rooms in building proceed to say no month over month and 12 months over 12 months. The whole of rooms in planning is rising, though at a decelerating tempo. Rate of interest development could trigger rooms within the planning part to fall within the subsequent few months.

Month-to-month P&L

U.S. resort gross working revenue per accessible room (GOPPAR) exceeded the pre-pandemic comparable for a fourth consecutive month. Every of the important thing bottom-line metrics, nonetheless, decreased barely from June, whereas whole income elevated with peak summer time room demand and revenues. Revenue margins had been stronger than July 2019 for each full- and limited-service accommodations, however GOP margins had been at decrease ranges than the earlier fourth months. The dip in margins will be attributed to increased bills related to extra ramped-up operations in addition to the overall rise in prices across the trade.

{kind=link}

Newest Weekly Knowledge

The week of 14-20 August confirmed a lower in room demand and occupancy, which is regular for this time of 12 months. Learn extra in our newest Market Restoration Monitor.

About STR

STR supplies premium information benchmarking, analytics and market insights for the worldwide hospitality trade. Based in 1985, STR maintains a presence in 15 nations with a company North American headquarters in Hendersonville, Tennessee, a global headquarters in London, and an Asia Pacific headquarters in Singapore. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), the main supplier of business actual property info, analytics and on-line marketplaces. For extra info, please go to str.com and costargroup.com.